The Trade Desk

Programmatic advertising, is this the future?

So.. what is The Trade Desk?

The Trade Desk (TTD) in its simplest form is a cloud based ad buying platform but there’s a lot more to it than that!

TTD enables its clients to execute advertising campaigns across all kinds of advertising formats including video (which includes connected TV (“CTV”)), display, audio, digital-out-of-home, native and social, on a multitude of devices, such as computers, mobile devices, televisions and streaming devices.

TTD is in the programmatic advertising game.

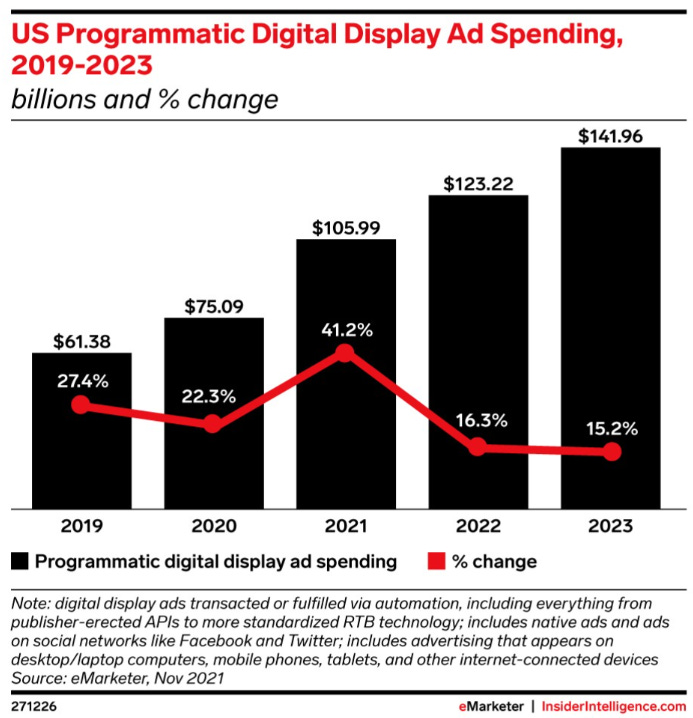

Programmatic advertising is the buying and selling of advertising inventory using algorithmic software that automates the process. TTD is jumping on the digital advertising bandwagon which has seen an increased shift particularly in the CTV space. CTV allows consumers to watch what they want, when they want and wherever they want. This gives content owners the ability to provide more relevant ads to viewers by leveraging the huge amount of data available to them. It’s new and over the last few years overall spend in programmatic has been increasing as shown by the below graphic from eMarketer:

TTD is team buyer.

It purely operates on the purchaser side of advertisements and avoids any conflict of interest by never representing the seller in any transaction. Historically this has been an issue in the advertising world where an ad agent would represent both the buyer and seller and be purely motivated by the transaction with a potential conflict of interest favouring one over the other.

Advertising has evolved in recent years as the advancement in algorithms, machine learning and the harvesting of data has improved at a rapid pace.

In the past advertisers were required to buy up bulk blocks of ad inventory well into the future meaning it was difficult to pivot if trends changed let alone value what that ad stock should be worth. In more recent times the emphasis on seeing a return on businesses advertising investment has grown and the need for advertising dollars going further is greater. Advertising has moved to live valuation of ad’s meaning ad buyers can bid on current slots in the short term rather than having to predict the future.

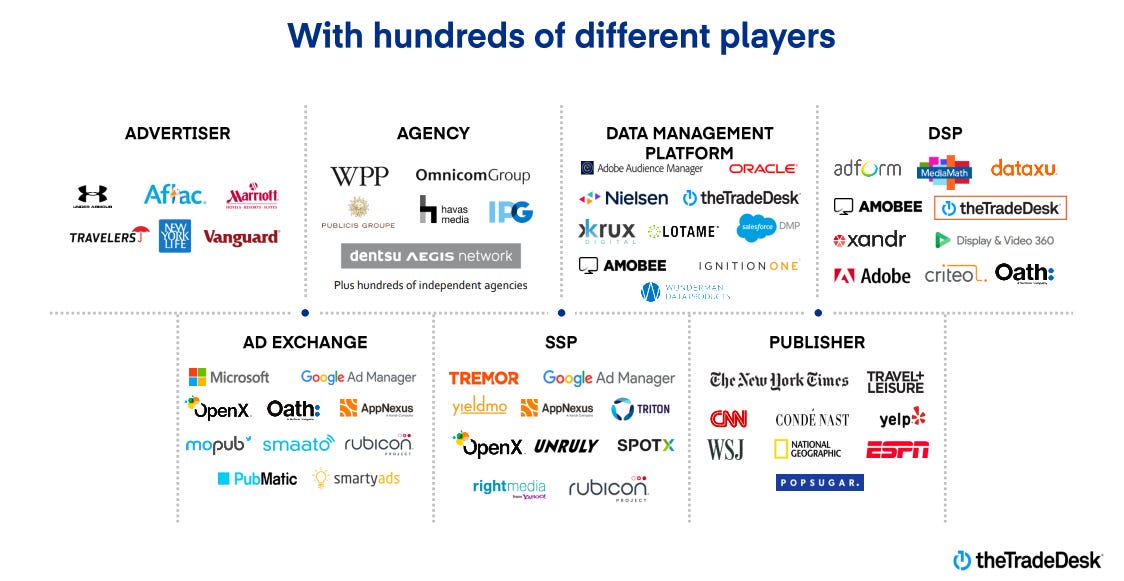

Ad inventory can now be sold on an ad-exchange and this is where TTD comes into play.

Think of a scenario where ESPN is an ad publisher with an ad slot available and would like to sell a block of advertising. ESPN would then work with a Sell Side Platform (SSP) which would control that inventory asset with the aim to get the most out of that block, offering it on an ad exchange and engaging with a Demand Side Platform (DSP) like TTD.

TTD uses its technology and the data it has accumulated to tailor its advertising to its clients.

Historically advertisers would bid on inventory regardless of the impressions that inventory would generate. Continuing with the ESPN example an individual watching ESPN and based on the data available to TTD may be more likely to be interested in health and fitness which therefore the ad slot may be more valuable to an advertiser like Under Armour than perhaps an investment vehicle like Vanguard.

TTD operates within an extremely competitive industry with some of the heavyweights of the world, in particular Google, Amazon and Meta (Facebook).

Google, Amazon and Meta are considered ‘walled gardens‘ which is a closed platform that handles all the buying, serving, tracking and reporting of the advertising.

Walled gardens restrict access to data as they see fit to control the market with the ultimate goal of creating a monopoly on advertising. TTD’s point of difference with these giants is that it isn't considered a walled garden and is a completely open platform. TTD enables ad buyers to utilise third-party data to measure advertising campaign performance and efficiency as well as manage and review campaign performance in real time.

TTD’s platform allows its clients to customise their own application programming interface (API) and build their own features on top of the TTD platform. Clients can then run their own reporting tools, strategy and algorithms to assess and maintain their advertising campaigns.

Competing with these behemoths brings risk.

With big budgets these businesses could potentially expand into TTD’s territory, further increasing competition or introducing a lower cost offering. According to TTD themselves there is limited cost and difficulty in moving ad spend to other competitors.

Okay.. How does TTD make money?

TTD generates its revenue by charging its clients a fee being a percentage of the total ad spend as well as providing data and other value add services purchased through the platform.

Clients enter master services agreements with TTD with one year auto renewing service agreements unless they are agreed to be terminated earlier. The price of the transaction of which the fee is based is determined by the price TTD expects to receive once the bid is won, which is essentially when a client purchases through its platform. Over the last three years TTD has had a client retention rate of over 95%.

TTD’s income is therefore reliant on client advertising spend.

A risk for TTD would be that a looming recession or downturn may mean that its clients look to reduce ad spend which would therefore lower the fees it can charge. It may also mean that businesses want to see a return on their ad spend and the platform TTD provides may give them the data and assurance they require to continue spending.

TTD has some concentration risk within its client base.

As reported in the most recent 10K filings, if all of TTD’s individual client contractual relationships were aggregated at the holding company level, Publicis Groupe would represent more than 10% of Gross Billings in 2022. In saying this, TTD had over 1,000 clients at 31 December 2022 which are primarily advertising agencies. These advertising agencies are often owned by holding companies although the decision making around advertising is generally made at the agency level and not by the holding company. There is still a risk that if a holding company is put off by TTD it could potentially lose those agencies.

When reviewing the financials one thing that really stood out to me was the high level of receivables vs total revenue.

While revenue for 2022 was $1.5B accounts receivable was $2.3B. Rest assured that it is purely a quirk in reporting. Revenue is reported as the net amount of total billings to clients less what is paid for the cost of the advertising inventory. Accounts receivable excludes the cost of the inventory although this portion is recorded in the accounts payable. Hence the reason both receivables and payables seem quite high!

Who runs this thing?

TTD was created by Jeff Green and David Pickles who both remain key leaders of the management team as Chief Executive Officer and Chief Technology Officer respectively.

It all began when Green and co sold their original business AdECN to Microsoft back in 2007. AdECN was an advertising exchange for buying and selling display advertising. Green then began to work at Microsoft which is where he met Pickles. In 2009 TTD was founded and later IPO’d in 2016.

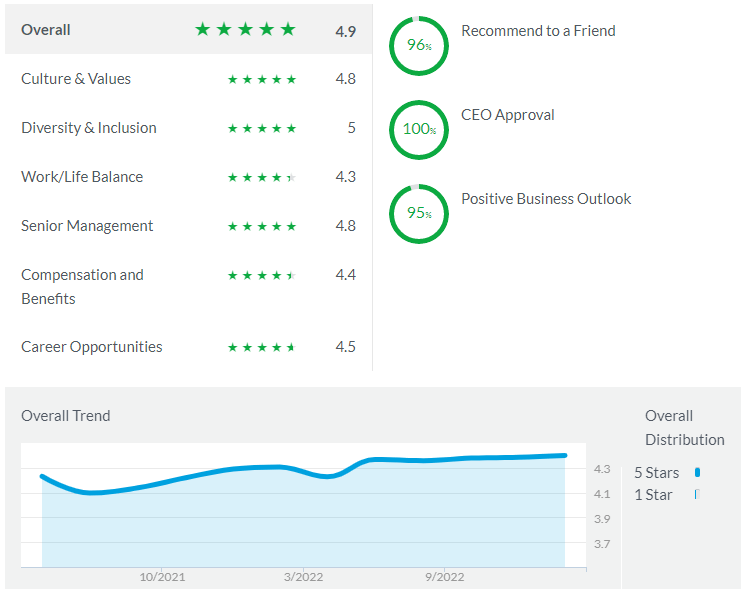

Glass door ratings can be hit and miss depending on the level of reviews.

Currently Green has a CEO approval rating of 100% although this is only off 9 reviews. TTD itself has an overall rating of 4.9 stars which is extremely high but again this is on the back of 383 ratings. Compare this to the other extreme where a company like Microsoft has 47K reviews and 9K reviews of its CEO Satya Nadella.

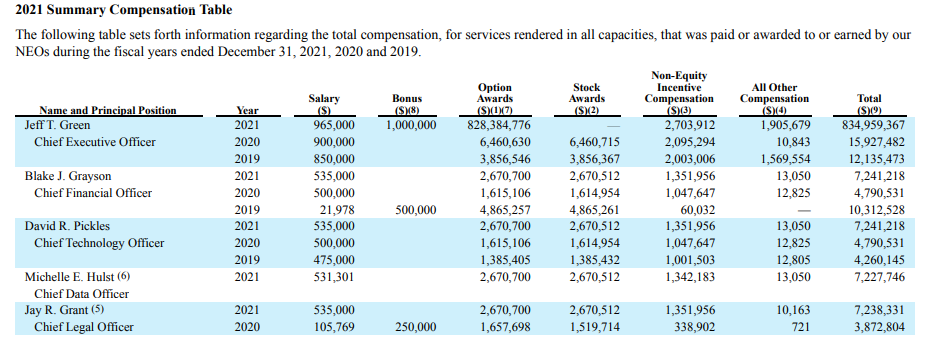

TTD has both Short Term Incentive (STI) and Long Term Incentive (LTI) compensation plans for its management team. The below covers what was released in the most recent proxy statement.

The STI targets included bonuses based on revenue reported for the year, the higher the revenue the higher the % allocated as a bonus. For example in 2021 the revenue target was $1,060M which had an associated bonus factor for CEO Green of 0.10094%. This would result in a bonus of $1,070,000 - 111% of his base salary. The STI payments are also made to the executive team which is again based on revenue but at a lower %. While it is great to see revenue growth and this is one way to incentivise that it does run the risk that management is solely focused on growing revenues and may be influenced to do whatever it takes to grow the topline and have less of a focus on becoming profitable.

This is where the LTI’s come into play.

The LTI’s at TTD are based on equity and therefore have a direct relationship with the stock price and therefore align with the long term goals of shareholders. Management is only rewarded when there is an increase in the stockholder value. TTD also uses multi year vesting to again align with longer term investors and therefore making it difficult for TTD management to cash out quickly.

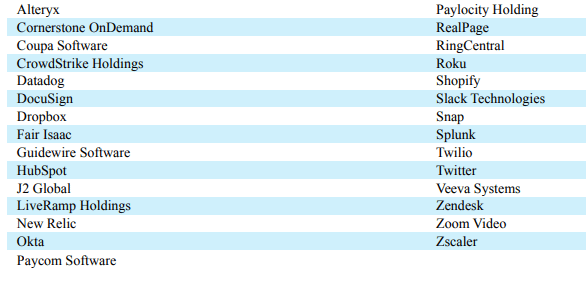

TTD’s management compensation is reviewed by its compensation committee.

The committee reviews compensation levels against TTD’s peers in similar industries of a similar size.

The companies in this compensation peer group were selected on the basis of their similarity to us, based on the following criteria:

publicly-traded companies headquartered in the United States;

similar industry and competitive market for talent (advertising, software, Internet software and services, IT consulting and services and research and consulting services);

similar revenue size – within a range of ~0.33x to ~3.0x our last four quarters’ revenue (approximately $200 million to approximately $2.0 billion);

similar market capitalization – within a range of ~0.25x to ~4.0x our market capitalization (approximately $6.7 billion to approximately $107.2 billion);

product and business model similarity;

high growth (greater than 20% growth over the last four fiscal quarters); and

high market capitalization to revenue multiple and high market capitalization to EBITDA multiple.

A list of these companies below:

You can hear the passion Green has for this business and particularly its employees when he speaks.

He is a significant asset to the business and with that comes the risk of losing him. If Green was to move on would TTD be able to fill the role with someone equally as passionate?

What $ does TTD make and how expensive is it?

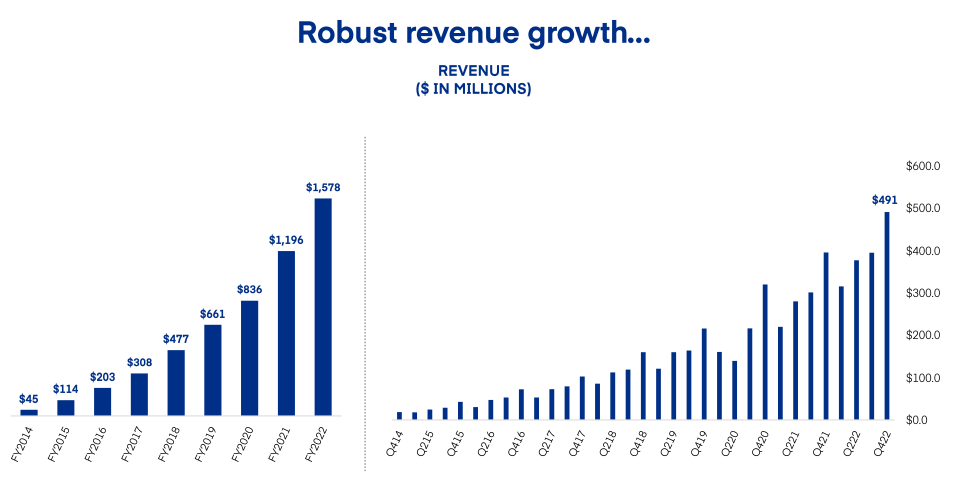

TTD has been a revenue growth machine

Excluding the pandemic impacted 2020 TTD has grown revenue at 30% + as well as expanding its gross margin from 76% in 2018 to 82% in 2022.

As meme form Chad Kroeger would say “look at this graph”....:

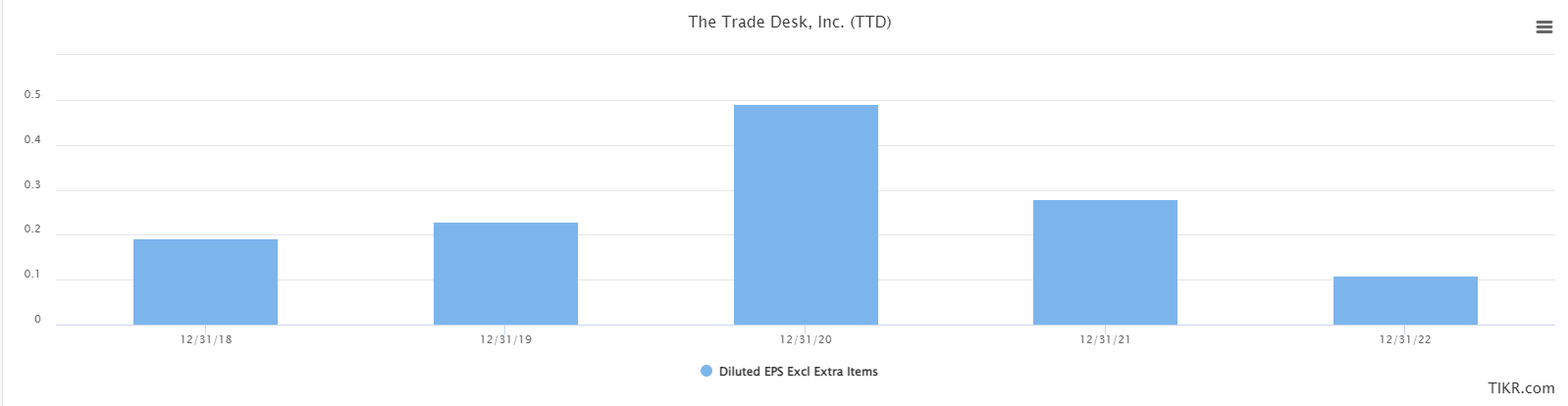

Unlike a lot of tech TTD has been operating at positive net income for a number of years now.

Net income over the past two years has been in decline on a per share basis as shown below:

So while revenue has been expanding at an impressive rate, expenses have been too.

Whether some of these costs could be pulled back if the company wanted to become more profitable is the question. 20% of TTD’s revenue was expensed on technology and development, investing back into the platform, excluding a small capitalised amount of around $7M shown on the cashflow statement. This reinvestment has been slowly growing over the past few years but has remained fairly consistent between 17% - 20%. Sales & Marketing has been consistently sitting at 20% of total revenue over the past few years.

The driver of the lower operating margin is the expansion of ‘General & Admin’ expense, which is primarily down to personnel costs.

Had the General & Admin expense remained at 20% of revenue as it was in 2020 and all things being equal TTD would be punching out a 20%+ operating margin (as it was in 2016-2018) compared to the 7.2% it had at 31 December 2022. The CEO performance option of $104M in stock based compensation was a big driver of this for 2022 and while management expects General & Admin to continue to increase into the future this doesn’t include a similar CEO performance option.

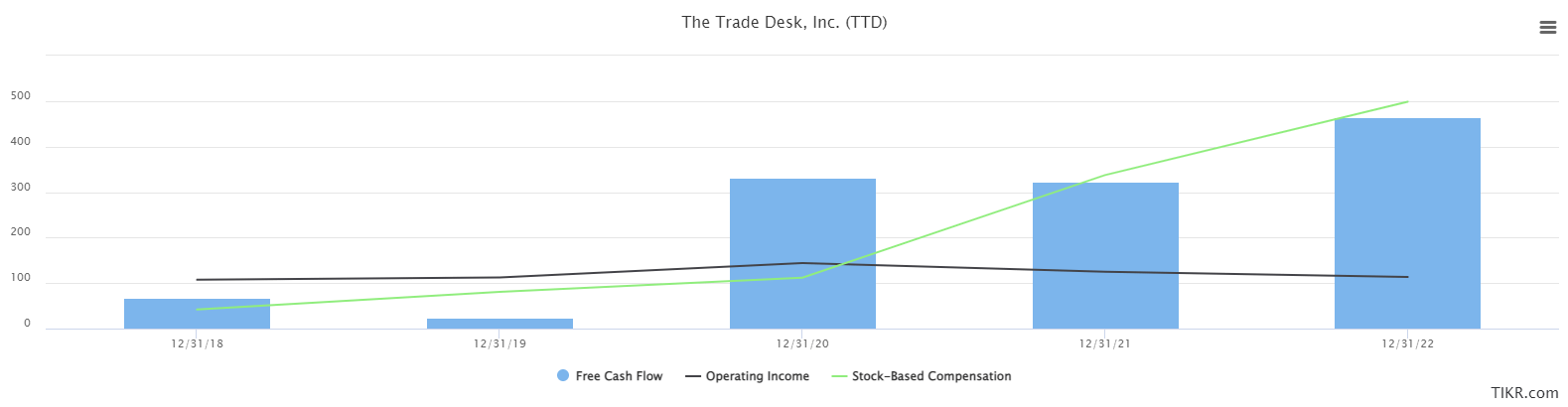

TTD is flushed with cash.

Its free cash flow margin has been hovering around 30% over the last few years and its free cash flow per share has been expanding. There is quite a disconnect between net income of the business and its free cash flow which comes down primarily to stock based compensation. As you can see the below graph shows that once the stock based payment tap was turned on cash flow kicked off, which makes sense:

The price you pay though for bulk cash is share dilution. The YoY change in the weighted average diluted shares outstanding was around 4% back in 2018 & 2019 and has fortunately dropped and in the 2022 financial year is down to an increase of 0.30%. In the most recent quarter TTD announced a share repurchase program to the tune of $700M which obviously helps offset part of the dilution.

From a valuation perspective TTD isn’t cheap..

Although if you consider what it was trading at during the free money festival of 2020 & 2021 it is at a relatively low point for the last three years. TTD’s price to sales multiple on its last 12 months is sitting at around 19x. At its peak in December 2020 it was 60x+!!. The Price to Earnings ratio can be a little risky to use on a company that has been growing at quite a rate with future results and growth likely baked into the price. Plus there is heavy reinvestment into the company which may be pushing the ‘E’ down lower than it could be. Having said that TTD’s trailing Price to Earnings ratio is hovering around the 550 mark.. Meaning that it has a lot of future growth required to justify the share price.

What next for TTD?

TTD is continuing to create an open internet and challenging its walled garden competitors.

In recent times it has created Unified ID 2.0 (UID2). UID2 is an unencrypted alphanumeric identifier created off of a user's email address or phone number. It enables advertisers to provide targeted content without the use of third party cookies. Third party cookies effectively track you across the web and are used by advertisers to provide targeted advertising which could be considered quite invasive of privacy.

In the most recent earnings call TTD was very bullish on the progress of UID2.

“If you had told me at this time last year, how much progress the industry would have made on UID2 in 2022, I don't think I would have believed you. At the beginning of our fourth quarter last year, around 15% of the third-party data ecosystem was estimating on UID2. This is essentially a very large sample of the entire data ecosystem of the entire Internet. By the first half of this year, we expect we will be in the 75% range. Levels of activation that high mean we will have effectively solved the identity matching challenge of the entire open Internet on a scale well beyond anything cookies have ever accomplished and all while providing consumers with much greater control over their privacy.”

Large companies such as AWS, Snowflake, Salesforce and Adobe were all adopting UID2.

TTD has now launched its Galileo product which integrates with UID2 allowing advertisers to connect data with their customer relationship management systems and customer data platforms.

I would then assume that by allowing UID2 to be open source it enabled widespread adoption and with the introduction of Galileo it would be logical that a business would then integrate Galileo into its tech stack.

The business has a strong network effect when it comes to data.

The more agencies using the platform the more data is available to TTD. The more data the greater information the algorithm has to create a better user experience and more effective ad campaigns.

In the short term, the first quarter of 2023 will be an interesting watch given the macro environment the world is dealing with.

In the most recent call management noted that they expect YoY revenue growth of around 15% in Q1 2023. It was also raised that operating expenditure would increase on a YoY basis (excluding stock based compensation) as TTD plans to increase headcount as well as return to a in person meetings and live events, increasing travel and associated costs.

Overall I believe the above outlines the strengths of TTD as well as some of the key risks and focus areas to watch as an investor. To me it feels expensive, but some of the best companies always do! If you’re still reading at this point I appreciate you! If you have any suggestions, critiques or guidance on what could be done better on the above I would greatly appreciate it. The above is all for research purposes only and shouldn’t be taken as advice!

Gracias!